How to process donations under the Gift Aid Small Donations Scheme (UK only)

Note

This Support Article should be read in conjunction with HMRC's guidance on Claiming Gift Aid as a Charity, and also HMRC's updated guidance on claiming GASDS from 6th April 2017, which has implications for multi-site churches claiming Gift Aid under the Small Donations Scheme for more than one site within the same Local Authority. Please check to make sure your organisation is eligible for reclaiming Gift Aid under the GASDS and that your financial admin procedures cater for proper record keeping and processing of donations eligible under the Scheme.

The Giving module includes a special "system-installed" giver profile for recording small donations against, called [Site], SDS - search within the Givers section for SDS. Multi-site customers will have a separate SDS giver profile for each site they create on their ChurchSuite account and, subject to HMRC rules and the location of each site, may be eligible for a Small Donations Scheme annual allowance for some, or even all, of their sites.

At the time of writing - from 6th April 2020 - HMRC permits qualifying organisations to claim Gift Aid up to £2,000 per qualifying site per tax year on qualifying cash or contactless donations with an individual donation value of up to £30 (or up to £20 donation value up to 5th April 2019). To prevent this limit from being exceeded, ChurchSuite keeps track of each SDS giver profile and caps the Gift Aid re-claim once the annual threshold is reached. While there is no limit to the annual total value of small donations that can be processed, ChurchSuite will only permit you to claim Gift Aid up to the annual allowance in any tax year.

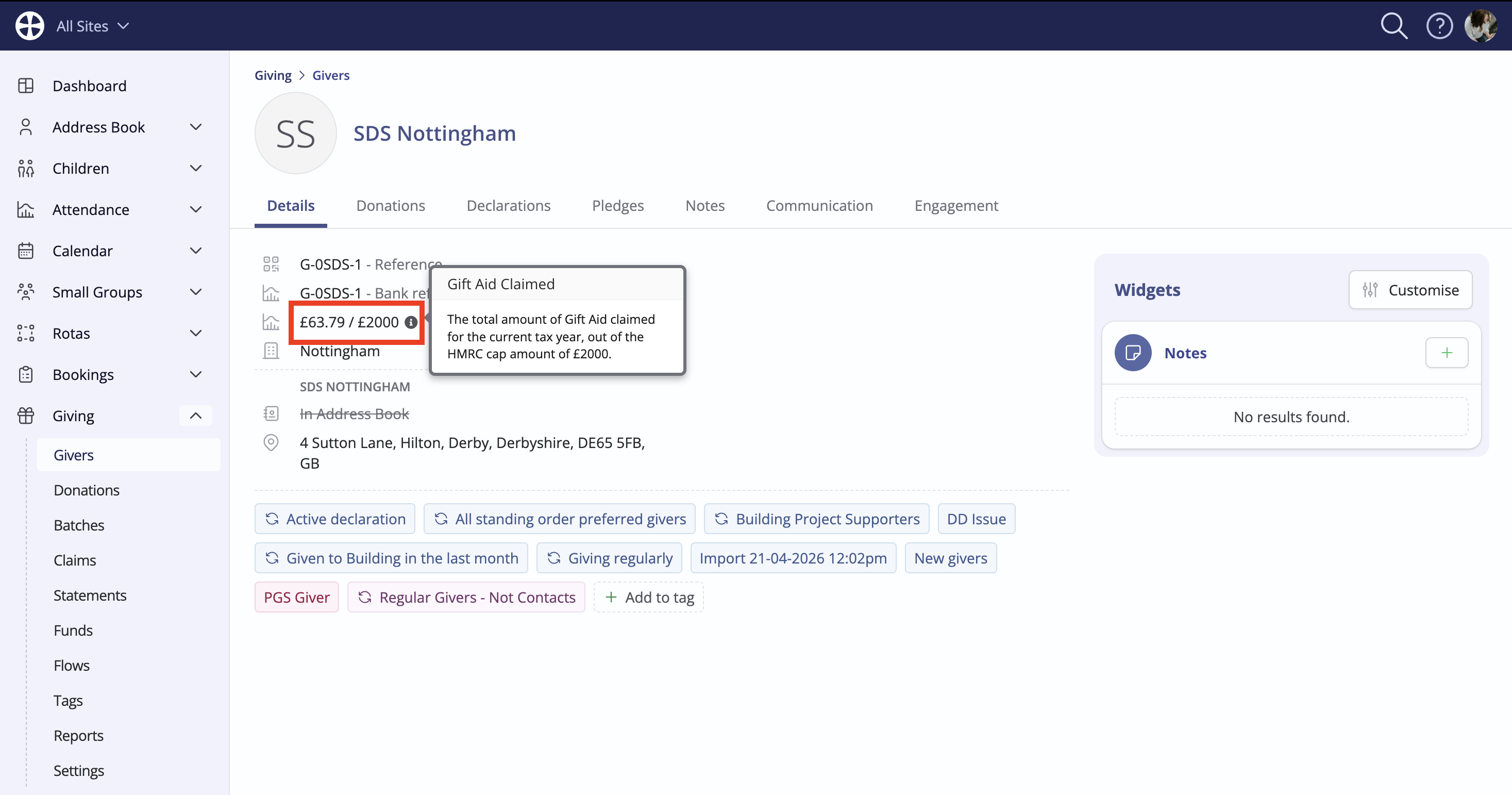

A progress indicator is shown on each SDS giver profile showing the total amount of Gift Aid already claimed for small donations in the current tax year - in the example below, the organisation has claimed £63.79 of its £2000 allowance for the current tax year.

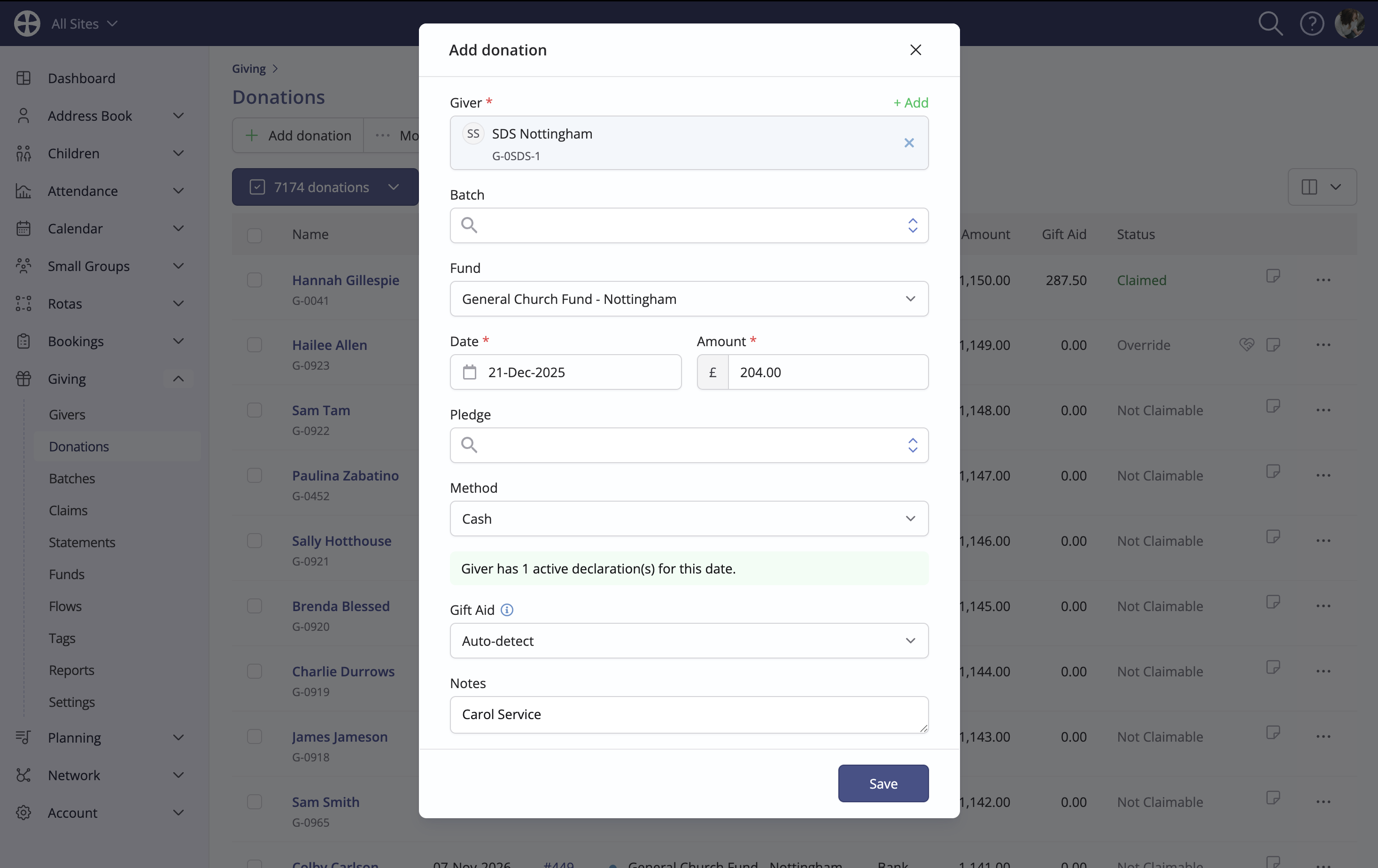

When adding donations to the Giving module, you'll search/select the SDS giver profile and complete the rest of the Add donation pop-up in the normal manner, taking care to only add donations eligible under the Small Donations Scheme.

Top Tip!

As you approach your annual allowance, it may be necessary to break larger bulk amounts of small donations into smaller amounts to claim up to the full annual allowance. For example, if you've previously claimed Gift Aid on small donations of £1,990 and the annual allowance is £2,000, you will need to break a large posting of small donations into two amounts - one small enough to obtain the remaining £10 of Gift Aid allowance and the other amount representing the balance of small donations.